A practical breakdown of the new R&D tax relief schemes, and how to identify where businesses may receive less under ERIS

The Enhanced R&D Intensive Support (ERIS) scheme is often presented as the most generous form of UK R&D tax relief, offering up to a 26.97% benefit on qualifying expenditure for R&D Intensive Loss-Making SMEs.

But the “up to” is doing a lot of heavy lifting in that sentence.

Under ERIS, the effective benefit rate can fall as low as 12.47% and therefore, in some cases, is less generous than the rate under the merged scheme.

Understanding when this happens is critical, not just for making sure you claim under the right scheme each year, but for planning R&D investment and optimising cash returns. Let’s investigate this a little further.

The Key Difference in the Scheme Benefits

For the purposes of this article, we are considering a loss-making SME who is R&D intensive. They can qualify for either the ERIS scheme or the Merged Scheme.

Merged Scheme

Under the merged scheme, the position is a net credit rate

For a loss-making SME you get a gross R&D credit which is worth 20% of your R&D expenditure. Even though you have no tax to pay, HMRC impose a fictional “notional” tax rate of 19% to bring the benefit in line with a profitable company for fairness.

This gives the company an effective rate of 16.2% per £1 spent on qualifying R&D expenditure.

ERIS Scheme

Under the ERIS scheme, you receive an R&D enhancement to increase your taxable losses. These losses can then be surrendered for a cash credit.

Qualifying companies get an enhancement of 86% based on qualifying R&D expenditure. When added to the original R&D expenditure, this gives R&D Enhanced Expenditure of 186% of the original spend.

Companies are then able to surrender the lower amount of the following for a cash credit at 14.5%:

- R&D Enhanced Expenditure

- Total available taxable losses

If a company has plenty of losses and are capped at the R&D Enhanced Expenditure, then it will receive a credit worth 26.97% of your R&D spend.

If a company doesn’t have sufficient losses, the credit will be worth far less than the 26.97%.

It could be as little as 12.47% of R&D spend. This is less than under the merged scheme.

When ERIS Can Be Worse

If a company has a very small taxable loss before the R&D claim, the taxable losses available will be less than the R&D enhanced expenditure.

Let’s have a look at how this can work in a couple of examples.

Example 1: Minimal Losses

- R&D spend: £100,000

- R&D enhancement: £86,000

- R&D enhanced expenditure: £186,000

- Pre-R&D taxable losses: £10,000

- Total available taxable losses: £96,000

A full surrender of total taxable losses for a tax credit at 14.5% will therefore provide a cash benefit of £13,920.

If the company had instead claimed under the merged scheme, they would have received a higher benefit of £16,200.

Example 2: Full ERIS Benefit Achieved

- R&D spend: £100,000

- R&D enhancement: £86,000

- R&D enhanced expenditure: £186,000

- Pre-R&D losses: £200,000

- Total available taxable losses: £286,000

The company can surrender the whole R&D Enhanced Expenditure for the credit at 14.5%.

This gives the company a cash benefit of £26,970. This is significantly more generous than the benefit received of £16,200.

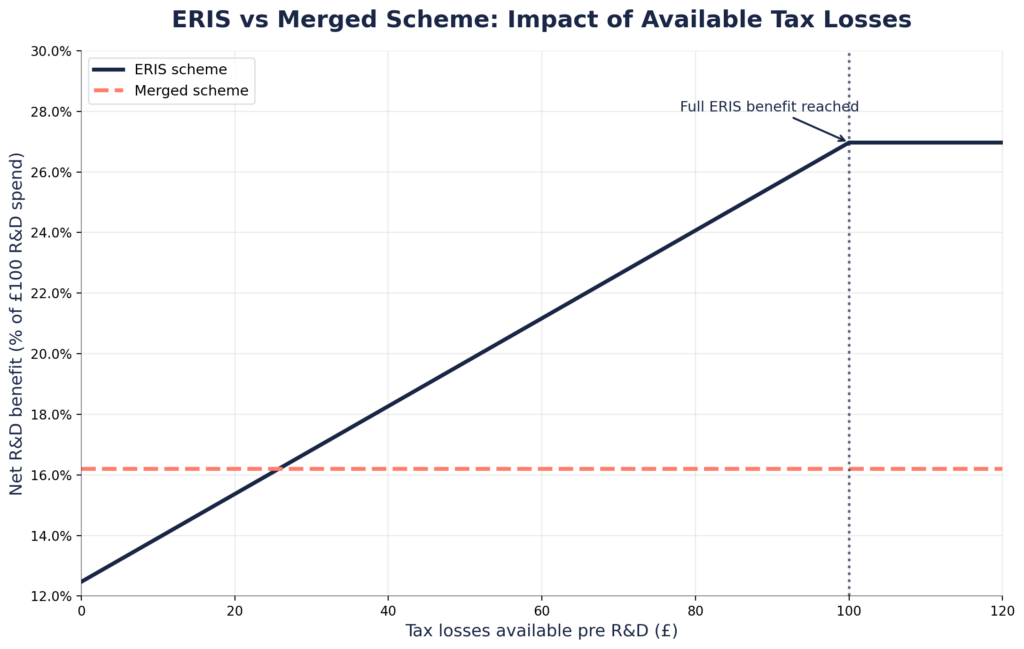

The Tipping Point

The breakeven point between ERIS and the merged scheme sits at having Pre-R&D taxable losses of roughly 26% of your R&D spend. If your losses are less than this level, then it might be beneficial to claim under the merged scheme. Above this level and ERIS becomes increasingly beneficial.

The chart above illustrates this tipping point.

It also illustrates that your effective R&D benefit rate will not be consistent. Additional losses change your R&D benefit rate at different stages.

- Low Tax Losses (below 26% of R&D spend) – ERIS benefit is 12.5% to 16.2%. Any additional losses at this stage don’t impact your cash benefit as you should be claiming under the merged scheme.

- Mid Tax Losses (between 26% and 100% of R&D spend) – ERIS benefit is 16.2% to 26.97%. Every additional £1 of loss increases your cash benefit by 14.5p.

- High Tax Losses (over 100% of R&D spend) – ERIS benefit is capped at 26.97% – Additional losses at this stage don’t impact your cash benefit as you benefit is already capped at the maximum benefit.

Good understanding of the this can mean that the timing of R&D and non-R&D investments becomes more important to ensure you are getting the most value out of your R&D Incentives.

Why Planning can matter more than you realise

Most people focus on eligibility for ERIS (loss-making SMEs who meet the 30% R&D intensity test), but eligibility alone does not guarantee optimal results for the company.

A company can be eligible for ERIS but still end up claiming under the merged scheme as it is more generous. However, as the ERIS benefit depends on losses at the point of claim, companies can influence outcomes through R&D investment and structuring decisions. For example:

- Timing of R&D Investment: If a company is expecting to be loss-making this year, but near breakeven or profit-making next year. Then accelerating R&D spend into the current period may unlock higher ERIS benefit. Despite the same R&D spend, delaying spend into a profitable period could reduce the total incentive benefit.

- Project Bunching: Instead of spreading R&D projects evenly across separate periods, a company may decide to group R&D projects into a single period to potentially qualify and maximise the ERIS returns.

- Managing the Loss Position: Since the ERIS benefit can improve as losses increase, depending where you are on the chart, companies may consider the following as examples:

- Bringing forward costs (e.g. bonuses, contractor payments)

- Taking salary instead of dividends

- Deferring revenue recognition where commercially and legally viable

So before defaulting to ERIS, businesses should ask:

- If considering in advance, is there anything we can proactively to improve our position?

- What are our losses before the R&D claim?

- Are we above or below the 26% threshold?